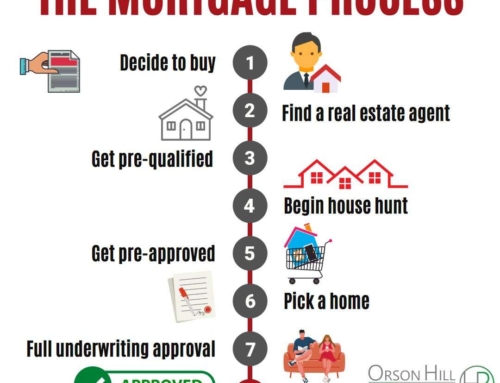

Pick the right mortgage lender or lose your dream home

You might notice when you first speak to your real estate agent that is helping you buy your him they mention lenders and home mortgages almost immediately. At least the good real estate agents do. There is a reason for this. Let’s first start by saying it is illegal for a real estate agent to receive any money or perk worth any value from a lender that they refer to you (unless that real estate agent is an MLO and most of us aren’t). So there really is no financial benefit to the Realtor for you to use that lender they refer. The reason that agent is sending you the names and contact information of lenders they know and trust is simple. They know that a lender can absolutely tank and destroy a deal faster than anyone else in that transaction. I have seen in the last two years more lenders screw up deals and not even apologies for doing so.

Many lenders do not care about the deal closing. They tend to not care about dates and deadlines and that attitude puts the buyer’s earnest money in jeopardy. I deal with lenders that are not responsive and just completely ignore the agents and the buyers for days and days just letting everyone in the transaction wondering if the deal is even going to close.

It is illegal for a real estate agent to receive any money or perk worth any value from a lender that they refer to you. There really is no financial benefit to the Realtor for you to use that lender they refer. Many lenders do not care about the deal closing and that attitude puts the buyer’s earnest money in jeopardy. I deal with lenders that are not responsive and just ignore the agents and the buyers for days and days just letting everyone in the transaction wondering if the deal is even going to close.

In a Seller's Market Who You Choose for a Lender Reflects the Strength of Your Offer

What that means is that in this incredibly competitive market (where there are multiple offers and some are cash on any given property) if a listing agent sees the buyer is using one of the big banks out of New York City they are seriously considering that offer weaker than one using a local lender (we will discuss the local lender below). Some buyers believe using the Bank of Americas, Wells Fargos and Chases make their offer better. There is nothing farther from the truth. When a listing agent sees those names on the lender letter they cringe. No one wants to deal with a bloated and huge conglomerate like that. If there is an offer that is the same with Bank of America as the Bank and one with Evergreen National Bank, The Evergreen National Bank offer is much more appealing and has a much better chance of closing and closing on time. That is just the things are. There is no arguing this simple fact.

The Lender's Excuse

Just Because You Know Someone at The Bank Doesn't Mean you Will Get Funded

Some people believe because they have a friend or relative that is a contact at a certain large bank they should use them. That is one of the biggest mistake buyers make. I have had so many clients regret using the bank their cousin works at. Some don’t close at all and some do not close on time. Remember in a seller’s market a seller does not need to postpone closing. They can snag your earnest money and then put the home back on the market and have under contract in 24 hours again. In this market you need to make sure you lender can perform and perform on time.

What Is the Solution?

I would never recommend not using a large bank for you mortgage without giving you a solution to this challenge. The best thing that any buyer can do is to use an MLO mortgage broker. This is a person that shops around (usually to reginal banks). The lenders that I refer to my buyers are hard working just like me. In this market if you see a home you like on Saturday you can not wait until Monday morning for your pre qual letter. You need that property specific lender that day to submit with your offer on Saturday night. Any lender that works 9-4 5 days a week will almost assure you not getting your offer accepted in this market. The lender I use I can text at 7 PM on Saturday and usually have a letter within 2 hours to submit with my offer.

Communication with a lender is key. The listing agent (the good ones anyways) will contact your lender prior to having their sellers sign the offer. They need to confirm you are a solid borrower. If they are unable to contact your lender they will pass you by and go to another buyer and not even look back.

just to Sum Things Up....

If your real estate agent refers you to a lender keep in mind they are not making money off that lender. They are only referring you to them because they know that lender knows local market conditions and that lender understands the challenges we run into with transaction in Colorado. It seems some lender do not like lending in Colorado for some reason. But others do. Always take the advice of you real estate in every aspect of the transaction including making sure you choose a lender that makes your offer look stronger and making sure that lender will perform within the confines of the contract. This includes dates and deadlines. Also choose a lender that will work the weekends and will give you their cell phone number. In this crazy market a 9-4 5 days a week banker will almost guarantee you will not win an offer over the weekend.

Leave A Comment

You must be logged in to post a comment.